Profitable growth in the consumer tissue value chain - where to look?

Written by Hampus Mörner, Christoph Euringer and Tino Mäkelä

Tissue producers are in a solid position, but the example of retailers expanding their private label offerings shows genuine interest in incorporating margins currently generated in the upstream business.

Ask any Chief Executive or salesperson about their unique selling point, and you will hear very different accounts of why their company is the best, the superior, or at least the one with the best outlook going forward. Citing the most value-added products, efficient production, the best service level, assets, etc. And within their individual sector, they might even be the leading company. But at the end of the day, there is a limited amount of money available in any value chain – and finally, only the distribution of profits should be the litmus test of who is performing best.

We had a look at the tissue industry, its key suppliers of fibre and machinery, and their main clientele – the big retailers and discounters. In short, the tissue industry has performed well, although the gap in value creation between the lower and higher end of company groups is notable. And yet, the key question for the tissue industry’s future is – how can it further improve its situation?

The simplified consumer tissue value chain holds four main company groups to enable the finished goods to end up at a consumer: pulp manufacturers, tissue paper producers, retailers, and machinery suppliers (including converting, pulp and paper and machinery equipment). Each group can be further divided and described in detail.

For instance, the stage consisting of tissue paper production can be divided between integrated paper producers (with converting capabilities) and independent converters (sourcing the base paper externally). Physical stores and traditional retailers may as well be replaced by e-commerce platforms. Moving forward, we will stay on the simplified level of breakdown.

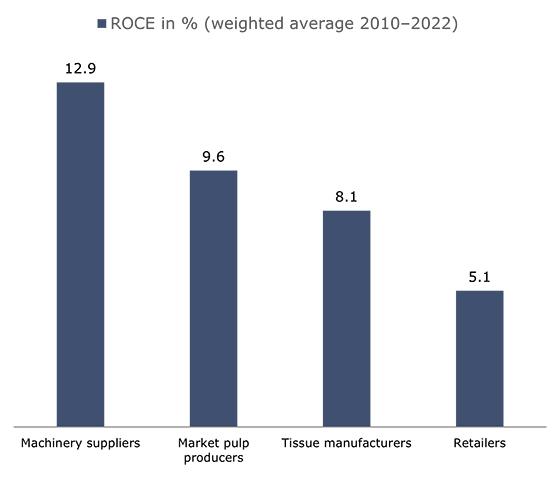

Figure 1 shows the average of ROCE between 2010–2022 as a weighted average (by turnover) for the selected steps in the value chain. The numbers are taken from the highest level of legal entity for the respective company and they basically also cover non-tissue businesses. Paper machine producers also sell packaging paper machines, tissue producers might have a non-woven business, and retailers have a very wide assortment. Still, on this helicopter level, it provides a robust picture of which type of companies are able to generate the highest profits.

Reading from Figure 1 and the comparison, the gap between the highest (machinery) and lowest level (retail) of value creation is notable. From the tissue industry perspective, the challenge comes more from the suppliers – they can achieve higher profitability levels – while retailers instead face stiff competition among themselves, and within this comparison, find themselves in the least comfortable situation.

What are the challenges within each of these groups?

Machinery suppliers: In Europe, this is a group of companies that have experienced a trend of growing consolidation historically and where few companies have led technology development. Many of the global top-tier players within this sector originate from Europe, leading in innovation and providing the highest technology level.

There have been numerous interesting acquisitions during the past few years, not only amongst the paper machinery and converting machinery suppliers but also recently across these two subgroups. Next to consolidation, the most recent acquisitions have also set a direction towards more complete end-to-end offerings where fewer parties are involved to fulfil an order for a complete line from stock preparation to packaging line. Technologies and solutions simply come under the control of fewer players.

Another aspect is the high thresholds to enter as a new machinery supplier. The business is capital-intensive, and being at the forefront of technology development and intellectual property is a decisive factor. Lastly, maintenance, training, diagnostics and any other services the incumbents can supply next to pure machinery purchases raise the entry bar further. Machinery suppliers have been successful in meeting the high demand for quality, energy efficiency, and strict environmental policies in Europe through their high – and specialised machinery know-how. This also carries a premium price.

Pulp suppliers: As the structural decline in graphic papers continues, tissue paper has become the single most important end-use segment for the market pulp sector. Essentially, this means that growth opportunities for pulp producers are more connected to the success of tissue paper when compared to the past.

Just as with the machinery suppliers, a positive aspect within the pulp sector is the increased consolidation witnessed in the last decades. Most global production assets are now under the control of a few leading corporations. Additionally, currently known capacity expansions are led by the top producers. Customers are facing fewer sourcing options and less bargaining power when buying pulp. Still, this consolidation and its impact on pricing power should not be overemphasised. It’s worth remembering that pulp remains a cyclical business, and prices were not kept from falling in the previous cycle.

Another supportive factor that has led to superior value creation is efficient resource management through land ownership, enabling access to competitively priced fibre, which is then converted to pulp in new mega sites. White spots on the global map show where the development of new pulp mills is becoming scarcer, and the need for access to land and massive CAPEX required for new modern “mega-mills” increases the thresholds. But it also drives producers to maximise economies of scale on the existing plots – and successful value creation.

Retailers: Reading from the comparison in Figure 1, this has been the company group creating the least value historically. Retail and grocery stores typically require high-priced real estate plots near consumers. Much of the store area is required for the traffic of consumers rather than shelves generating revenue. The number of goods that major retailers carry and handle can easily be counted in thousands, each requiring different space, shelf time and indirect cost to generate value finally.

Tissue articles make up a fraction of the total number of articles and are not necessarily the largest focus. On the other hand, tissue products are bulky and demand substantial shelf space. But as they are an everyday necessity, tissue paper products can, among other consumer goods, be a determining factor in driving traffic and, ultimately, consumers to stores.

Consequently, tissue is not only a product that claims much attention in stores but also a product any retailer is expected to offer. Given the importance of such an important item, where the cost of production is tied to the fluctuations in fibre and energy, and thus price volatility, retailers have for many years been tough negotiators to protect the value created from these vital articles.

They have also pushed for more private label (PL) products on their shelves. The growth of private labels has been distinct in the last decade, and reading from consumer panels from last year and onwards, there has been a growing trend in the form of more attention on “affordable” or “discount-oriented” brands on the costs of tissue producer brands. It is a fair assumption that the tissue industry might expect more pressure and push for PL as the retail group seeks to improve its value creation.

Tissue manufacturers: The group of tissue manufacturers comes out as the second lowest in the above comparison. Still, it is well within the range and at a level that can be considered acceptable. On the other hand, it is also at notable levels below machinery and pulp.

Unlike machinery and pulp, the European tissue sector has been the subject of fragmentation instead of consolidation during the last decade. Resilient, stable demand and bulky products make local presence key and have been supportive factors for investments by numerous stakeholders of varying scales. The total manufacturing footprint of the producers spans domestic and global players. Additionally, a prolonged period of low-interest rates has lowered the thresholds to enter until recently. Essentially, competition is up, which, in combination with an increased presence of sizeable discounters in the retail sector seeking higher value creation, has made it more challenging to obtain sustained long-term value creation.

Tissue producers are in a solid position, but the example of retailers expanding their private label offerings shows their genuine interest in incorporating margins currently generated in the upstream business. As the suppliers are further improving their position, one of the key questions for the years to come is if we are also going to see higher levels of consolidation in the tissue industry and what that means for the whole supply chain.

This article was originally published on the Tissue World Magazine website on 15 January 2023.

Bioindustry Management Consulting

Our service offerings, from corporate strategy to process design and from market insights to operational efficiency backed up by an understanding of best practices, detailed in-house databases, and analysis led by experts in the field, ensure your outstanding performance. We want to be your trusted partner.